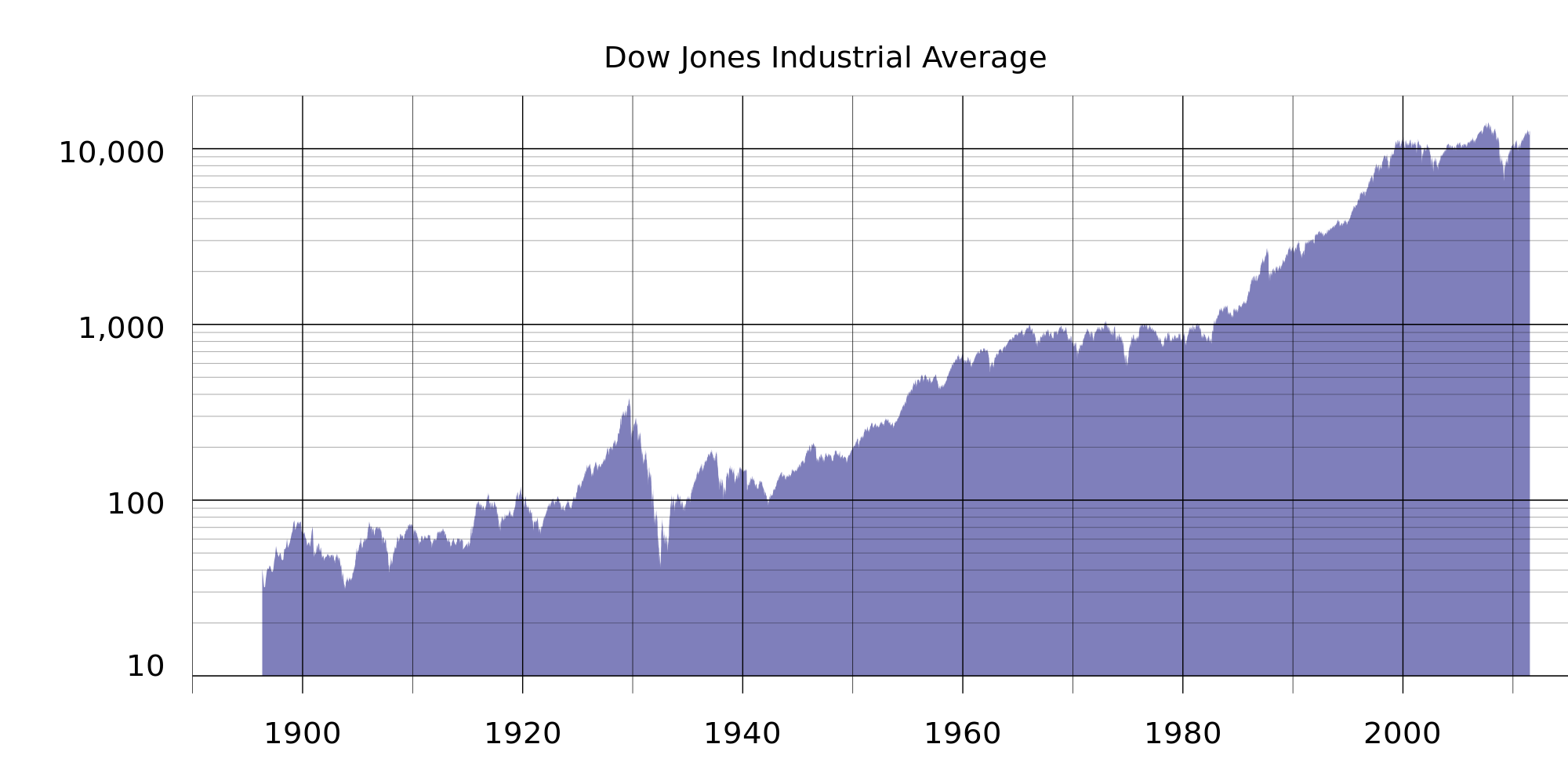

As @DarNoor; said, investing in individual stocks is usually a losing game. The best is to invest in actual index funds with low management fees. This is the what the stock market has looked like since it's inception:

As you can see, the stock market itself has always gone up, regardless of market crashes. Because of this, it's always provided a proper 7% increase on average over the long term. This is why it's statistically better to just put your money into an index fund, which basically invests in EVERY stock at once (most self made millionaires on a regular salary usually suggest a ratio of 40% bonds, and 60% stocks over 20+ years, and that 60% usually consists of half a US index fund, and half an international fund).

Interesting facts:

- Close to 90% of mutual funds fail to beat the market average of 7% over the long term. So any financial adviser that says "Well this fund will beat the market so invest in this one! And it's been beating the market for years!" is complete bullshit. Ask to see the record of him investing in that fund since its inception, which we won't be able too. Hindsight is 20/20.

- Most hedge fund managers of big corporations, usually just invest in index funds. They're not picking any super special stocks.

- It's VERY hard to beat the market. In order to profit well from it, you need to get very lucky, or you need to be better than everyone else at predicting the value of a company. And that's a full time job. A stock has most likely adjusted because of its worth when you hear a "hot stock tip". Even Warren Buffet recommend everyone just invest in index funds.

- Management fees are big things that people often overlook. For index funds you should be paying less than 1%. Note that just a 1% increase in management expense ratios can mean 5 to 6 digits of lost investment potential over a couple decades.

- Pay debts off first unless it's a low interest rate mortgage or line of credit (like 3%). If you're getting a 7% gain, but 15% debt, you're losing money. It makes no sense to invest until that debt is paid off (it will make sense if you do the math with compounding the interest). Even if you wait to invest, and pay the car loan off first, you will still make more money then if you tried to invest now partially while paying off your car loan slowly.

- Register your investments in a gov. retirement account. I don't know that the international equivalent is, but in Canada it's an RRSP, and in the US it's a 401K. The is money that becomes a tax write-off at the end of the year, so you'll get big tax returns. Whatever returns you get, re-invest them back into your account for next year. This will compound your investments, getting you rich quicker.

- Find whatever way you can to put money into your investments in the beggining (but don't take out a loan). The more money you can put into your investments into the beginning, the faster it will grow.

")